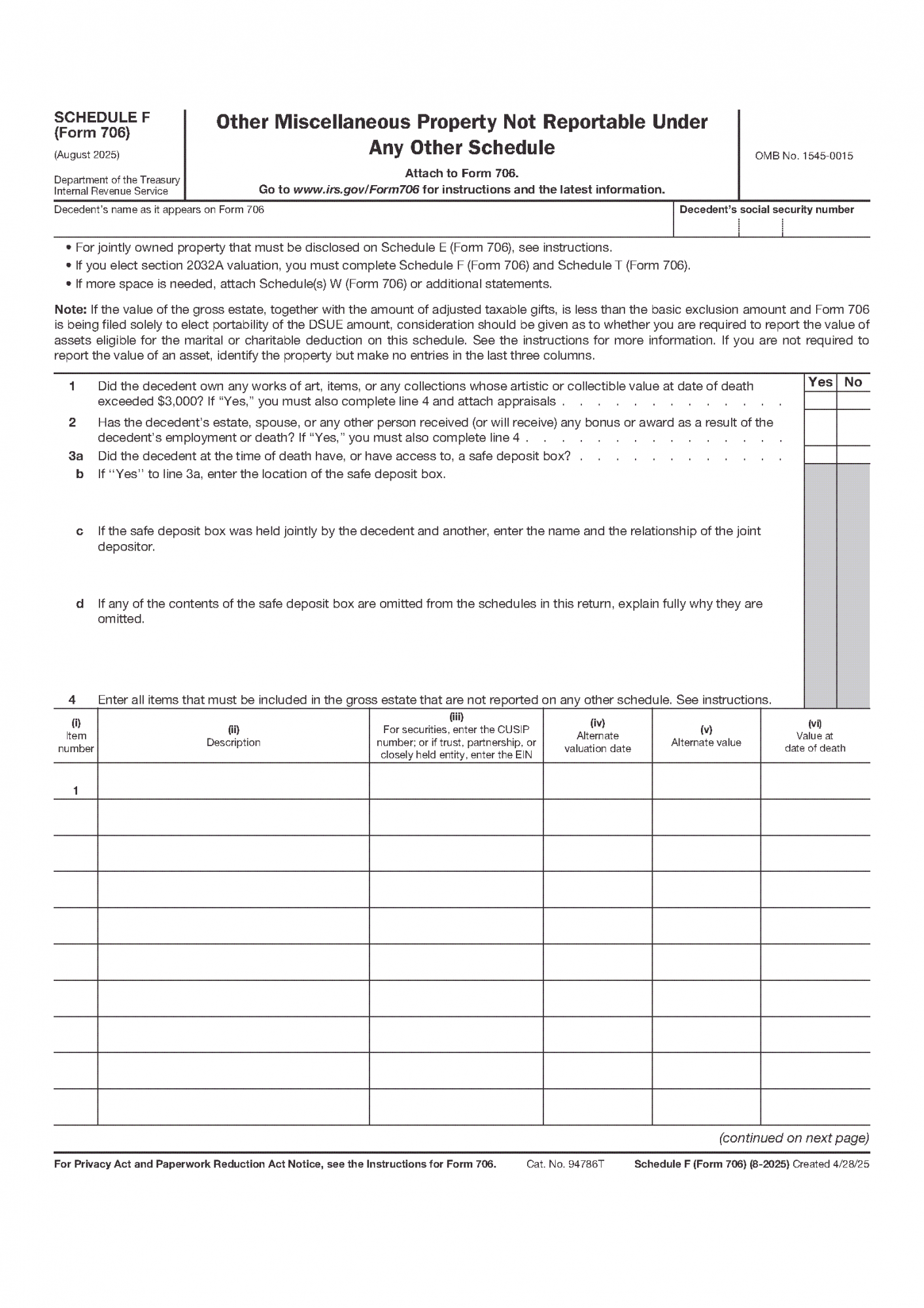

Schedule F is used in the Form 706 process to report property interests that do not fall within the specific asset categories addressed by other schedules. These interests may vary widely in form and legal character, but they are included because the estate tax system requires a complete accounting of all property connected to the decedent at the time of death.

Why certain assets are reported as other property

The estate tax system relies on categorical schedules to apply appropriate valuation and inclusion rules. When a property interest does not meet the definitions of real estate, securities, cash, insurance, or other specifically enumerated categories, it is reported as other property so the system can still evaluate its contribution to the gross estate.

The formal structure of Form 706 and the placement of each schedule within the return are defined on the IRS Form 706 document page.

Types of property commonly included on this schedule

Other property may include tangible personal property, intellectual property interests, business-related rights, or contractual interests that were owned or controlled by the decedent. Inclusion depends on whether the interest represents an economic benefit that is attributable to the decedent at death under estate tax rules.

Because these assets often involve individualized facts, their classification reflects how the system measures ownership and control rather than the form of the asset itself.

Valuation of other property interests

For estate tax purposes, other property interests are valued based on their fair market value as of the date of death or an alternate valuation date when applicable. The valuation method depends on the nature of the interest and the availability of market or appraisal data.

The values reported on this schedule flow into the gross estate and influence later deductions and tax calculations.

Interaction with deductions and estate reductions

Property reported on this schedule may be subject to debts, expenses, or claims that reduce the estate at later stages of the Form 706 process. These reductions are applied after asset valuation as part of the system’s structured approach to determining the net taxable estate.

The application of these reductions is described in estate expenses and debts under Form 706.

How this schedule fits into the overall Form 706 process

The reporting of other property interests represents one stage in the broader Form 706 filing sequence. Once these assets are identified and valued, the estate proceeds to integrate remaining property categories, apply deductions, and calculate the final estate tax outcome.

The position of this stage within the complete filing sequence is described in how the Form 706 filing process works, while the central overview for all Form 706-related scenarios is available in the Form 706 overview.